| Financial Planning | Budgeting | Saving | Investing | Retirement | Senior Living Costs | Real Estate | Interest Rates | | Inflation (CPI) Charts |

|

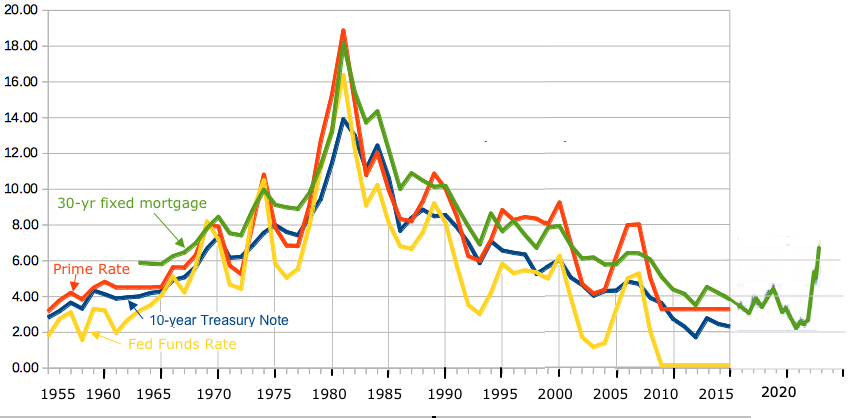

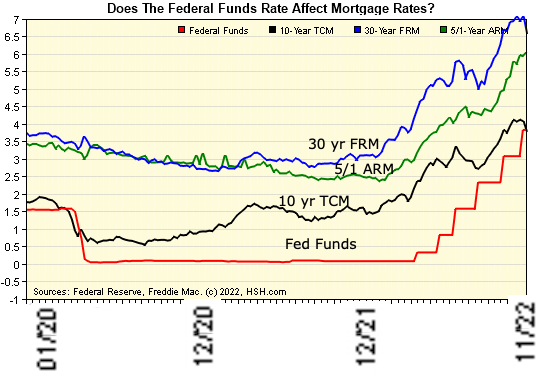

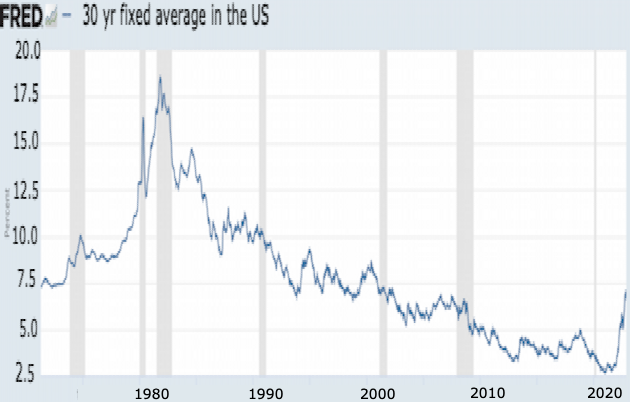

Mortgage Rates:

Simple loan payment calculator | BankRate

Historical: as of Nov 20, 2022

Last 3 months at hsh Click on Rate Graph 30-Year Fixed-Rate Mortgages Since 1971 - FreddieMac Fixed Income - CDs - Bonds - Treasury bills January 2019

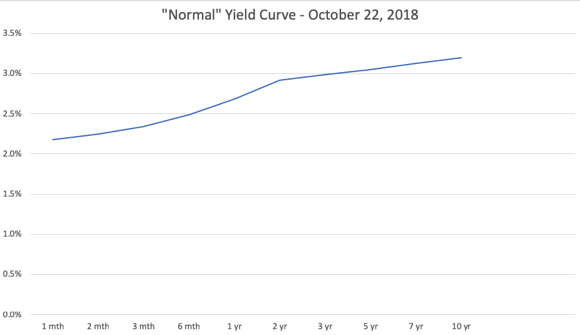

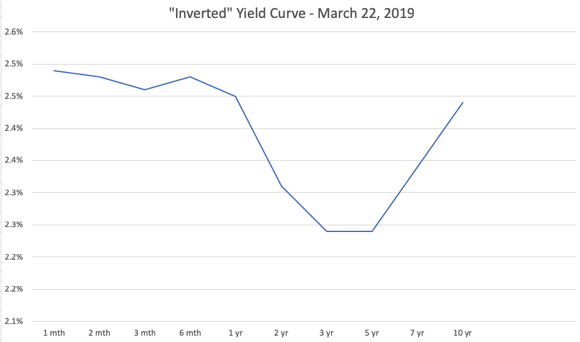

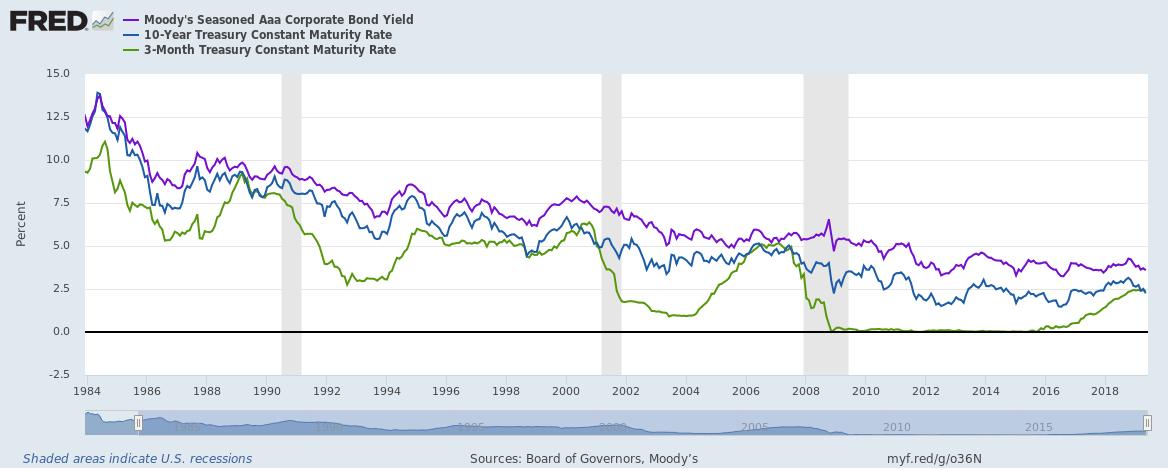

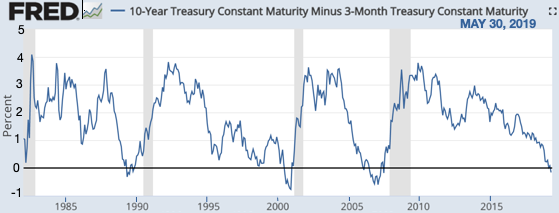

† S- Taxable State (In states which have income taxes) † F- Taxable Federal * zero-coupon bonds, do not pay a regular coupon. Instead, they are sold at a discount to their face (or par) value. ‡ government-sponsored enterprises (GSEs), which are federally chartered corporations but publicly owned by stockholders Source: Fixed Income & Bond Yields - Fidelity 30-Year Treasury Constant Maturity Rate | FRED | St. Louis Fed Inverted yield curve:

At The Impact of an Inverted Yield Curve Mar. 2019, Investopedia says,

Historically an inverted yield curve has been viewed as an indicator of a pending economic recession. Fortelling a fall in long-term fixed income yields.

Why:

The effect: More recently, this viewpoint has been called into question, as foreign purchases of securities issued by the U.S. Treasury have created a high and sustained level of demand for products backed by U.S. government debt. While experts question whether or not an inverted yield curve remains a strong indicator of pending economic recession, keep in mind that history is littered with portfolios that were devastated when investors blindly followed predictions about how "it's different this time." What it does signal in the short term is likely stop in raising rated by the Fed and a possible lowering of the federal funds rate.

Ken Fisher, wall street analyst and financial advisor, says,

The rapid fall in rates is more of a concert. It means there is more demand for fixed rate investments over securities. T-bill rates: T-bill rates are determined by Treasury auctions, which occur weekly for short term rates. 1 year and longer maturity rate auctions are held monthly. There are 23 authorized primary dealers that include institutional investors, including banks, broker/dealers, investment funds, retirement funds and pensions, foreign accounts, insurance companies and other organizations. The higher the yields on 10-, 20- and 30-year Treasuries, the better the economic outlook. Terms: The federal funds rate is the primary tool that the Federal Open Market Committee (Fed) uses to influence interest rates and the economy. The interest rate at which banks and other depository institutions actively trade balances held at the Federal Reserve, called federal funds, with each other, usually overnight. Changes in the federal funds rate influence the borrowing cost of banks in the overnight lending market, and subsequently the returns offered on bank deposit products such as certificates of deposit, savings accounts and money market accounts. Prime Rate - The rate at which banks will lend money to their most-favored customers. The Wall Street Journal surveys the 30 largest banks, and when three-quarters of them (23) change, the Journal changes its published prime rate.

Treasury bills, bonds, and notes are debt instruments that the government issues. 10-Year Treasury Note - A debt obligation issued by the United States government that matures in 10 years. A 10-year Treasury note pays interest at a fixed rate once every six months and pays the face value to the holder at maturity. The interest payments are exempt from state and local income tax. However, they are still taxable at the federal level. Treasury Notes can be sold before maturity. If the interest rates have gone up the value will be lower than the face value. If interest rates go down the value will be higher. T-bill - A short-term debt obligation backed by the U.S. government with a maturity of less than one year. Commonly have maturities of one month (four weeks), three months (13 weeks) or six months (26 weeks).

Mortgage Rates:

Mortgages come in several vareties.

Term - Typically 15, 20 and 30 years

Fixed Rate - Rate is the same for the term of the mortgage.

ARM - Adjustable Rate Mortgage.

FHA - A mortgage insured by the Federal Housing Administration. Borrowers with FHA loans pay for mortgage insurance, which protects the lender from a loss if the borrower defaults on the loan.

APR - Annual Percentage Rate - The interest rate for a whole year (annualized), rather than just a monthly fee/rate. It is slightly higher than the nominal rate, Because of compounding the bank gets more when you pay each month rather than hang on to your money until the end of the year.

Points - A % paid up front at the time of the loan.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||